Microfinances & Alternatif Scoring in Africa : A Modern Response to Credit Risk Challenges

On the African continent, Microfinance Institutions (MFIs) play a central role in the financial inclusion of populations excluded from the classical banking system, from informal entrepreneurs to low-income workers. Despite progress, according to RFI, nearly 60% of the African population remains without a formal bank account, limiting access to traditional financing.

The challenge is therefore twofold:

- How to rigorously measure credit risk in the absence of traditional data?

- And how to turn this constraint into a driver of inclusive and sustainable growth?

This context pushes institutions to explore innovative approaches, where alternative scoring and artificial intelligence (AI) become essential catalysts to expand access to financing, particularly in microfinance and digital banking services.

We will address the following questions:

- What is the current context of microfinance in Africa?

- Why do traditional scoring models fail to serve informal populations?

- What is alternative scoring and how does digital data change the game?

- What is the role of AI and advanced technologies in creating these models, and what risks and safeguards should be considered?

- What operational and strategic benefits do these innovations bring to financial institutions, banks, fintechs, and MFIs?

- What technical-strategic and operational recommendations ensure a successful transition to these evaluation methods?

1. Context & Challenges of Microfinance in Africa

According to Global Findex, the combined account ownership rate (bank accounts & mobile money) in several African markets remains significantly below that of developed countries, even though improvement is visible year after year.

According to Afriveille, in the WAEMU (West African Economic and Monetary Union), more than 19.7 million clients were served by 533 MFIs as of March 2025, representing a growth of over 6.9% in client numbers year-on-year. However, the average loan amount per client is decreasing, and the non-performing loan rate reaches 9.8%, well above the regulatory threshold of 3%.

According to We Are Tech, mobile money has exploded, with 40% of African adults holding a mobile money account in 2024, a global record, but only 7% use it for borrowing via these services.

These figures reveal a paradox: financial inclusion progresses in savings and payment services, but access to credit remains limited, mainly due to the lack of formal financial history for a large part of potential borrowers.

In summary, MFIs are essential to financial inclusion in Africa but face a major structural challenge: evaluating credit risk in a context lacking classical financial data. The real obstacle is not just the absence of data but the absence of a decision-making framework capable of leveraging non-banking signals, which MFIs still struggle to integrate into their traditional workflows.

Nexfing Recommendation:

Invest in data-driven R&D and pilot hybrid models combining traditional scoring and alternative scoring to strengthen credit decisions.

2. Why Traditional Scoring Models Fail

It should be recalled that these evaluation frameworks were designed for highly formalized economies, where incomes are declared, financial flows are tracked, and credit behaviors are relatively homogeneous. The reality of many African markets, marked by the informal economy, massive use of mobile money, and low penetration of traditional financial services, creates a structural gap between available tools and actual borrower behaviors.

- Limitations of Classical Banking Models :

Traditional models rely mainly on:

- Loan history,

- Previous repayment,

- Certified and fixed incomes,

- Stable employment status,

In many African markets, according to The Business & Financial Times, less than 30% of adults have a formal credit history detectable by traditional offices, meaning that 70% or more of the population has never had a financial product allowing banks to track repayment behavior, rendering most of these models ineffective or non-predictive.

- Deficit of Classical Banking Data :

The growth of mobile money generates digital transactional flows, but these data are not yet integrated into classical banking models. Their absence partially explains the persistence of a large segment of the population considered « credit invisible, » according to Further Africa.

Classical models can be described as « rigid architectures, » effective only in stable, formal environments. In a diversified African context, analytical agility outweighs methodological rigidity.

Nexfing Recommendation:

Adopt a hybrid scoring architecture combining banking history + alternative data + dynamic behavioral signals to improve scoring granularity.

3. The Role of Alternative Scoring: Innovation & Relevance

What is alternative scoring?

Alternative scoring relies on the analysis of non-banking or digitally native data: mobile money transactions, bill payments, telecom data, digital behavioral traces. AI allows extracting robust solvency prediction patterns from these unstructured datasets, even without classical history.

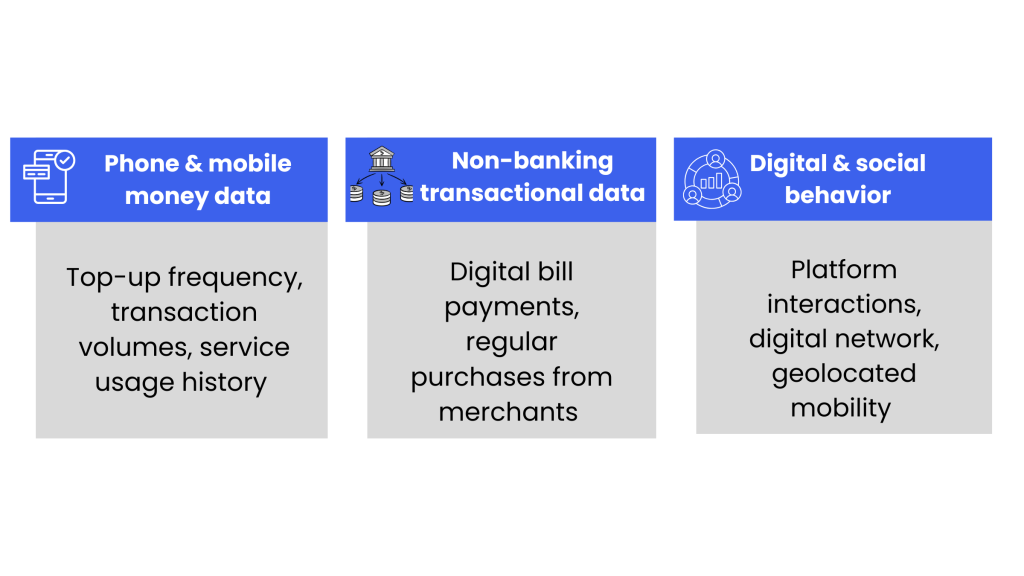

Alternative data sources :

Among the most relevant sources for African microfinance:

These models allow digital platforms to offer microloans within minutes without physical collateral, transforming the credit landscape in previously inaccessible markets.

Strategic role of AI :

The integration of AI, machine learning, predictive models, neural networks, captures nonlinear relationships between these alternative signals and actual repayment behavior. A recent McKinsey & Company report shows that 64% of financial institutions attribute revenue growth to the use of AI in risk and operations.

Alternative scoring is not just a substitution: it is a methodological revolution. It transforms discrete signals into quantitative risk metrics, increasing the ability to segment populations and anticipate default probability with high precision.

Nexfing Recommendation:

Deploy AI-native platforms with robust data pipelines (ETL, feature stores, ML Ops) integrating alternative data and scoring models for enhanced predictive reliability.

4. Technological Synergy: Microfinance & Data Science

Combining microfinance and alternative scoring is no longer theoretical but a strategic necessity to expand credit access while managing risk.

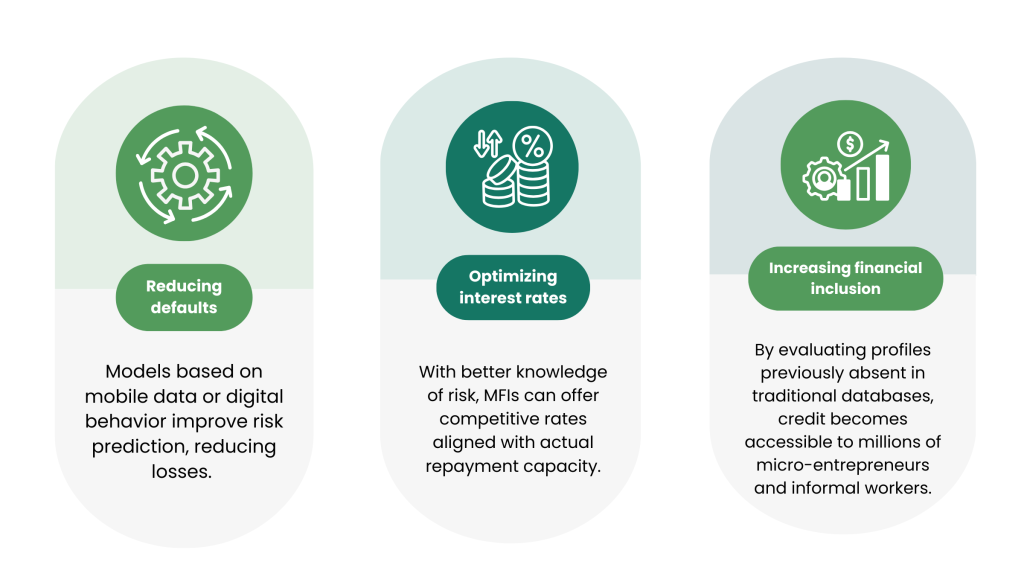

Objectives and concrete benefits:

Finally, the integration of technologies like AI and blockchain is emerging as an accelerator to secure data and automate credit decisions.

5. Use Cases and Recent Statistics :

Alternative scoring innovations have allowed several fintechs and MFIs to reach previously underserved segments, notably via mobile money, according to Further Africa.

In The Business & Financial Times, countries like Ghana are experimenting with hybrid models combining mobile money and social data.

According to OECD, in Ethiopia, AI-driven credit access financed more than 380,000 SMEs with a total of USD 150M.

These cases demonstrate that alternative scoring is not theoretical: it is an operational application with measurable benefits for inclusion and credit volumes.

An Essential Evolution :

Financial inclusion in Africa today depends as much on innovation as it does on traditional policies. Microfinance, relying on alternative scoring and digital technologies, is redefining the relationship between unbanked information and credit decisions. The challenge is clear: to transform the invisible informal economy into a predictable financial trajectory.

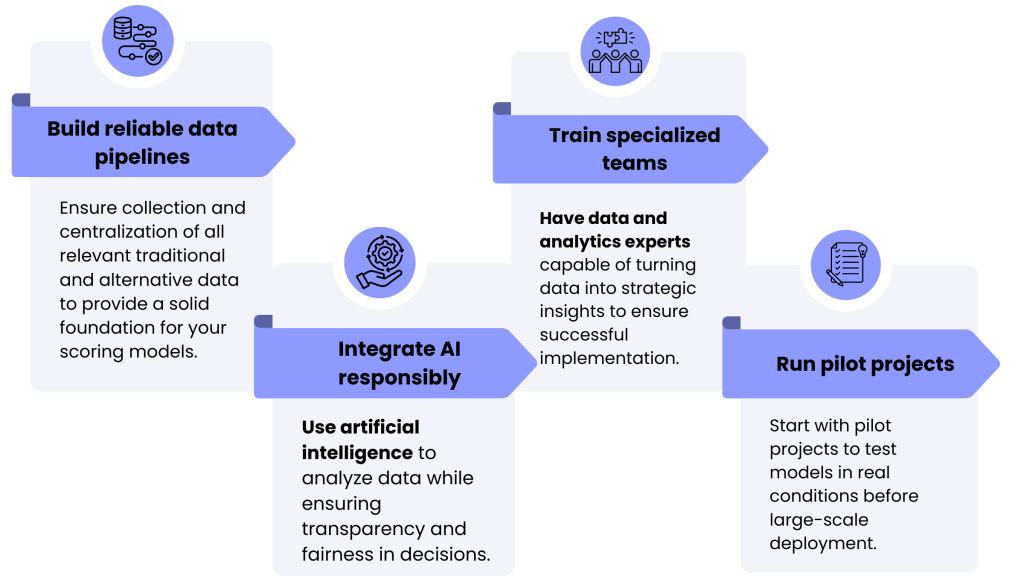

6. Recommendations for Successful Adoption of Alternative Scoring

What if Nexfing helped you build an alternative scoring model tailored to your needs?

With a dual expertise combining advanced technology and a real understanding of local African markets, Nexfing designs custom scoring solutions, perfectly adapted to microfinance needs and operational specifics of the continent.

By combining data science, AI, and behavioral analysis, our experts develop robust scoring models adapted to underformalized environments and compliant with regulatory requirements.

Objective: Provide microfinance institutions with more precise, inclusive, and business-aligned risk assessment capabilities.

Ready to move to smarter, more adapted scoring?

Contact Nexfing for a free consultation and accelerate your digital transformation.

Sources :

Afriveille : https://afriveille.com/microfinance-dans-lumoa-entre-collecte-record-et-fragilite-du-credit-au-1er-trimestre-2025/

We Are Tech : https://www.wearetech.africa/en/fils-uk/news/finance/digital-savings-soar-in-africa-but-mobile-credit-stalls-world-bank-finds

OECD (Organisation de Coopération et de Développement Économiques) : https://www.oecd.org/en/publications/africa-capital-markets-report-2025_7d26e1d3-en/full-report/harnessing-ai-in-finance-for-financial-inclusion-in-africa_a048b4fb.html

The Business & Financial Times : https://thebftonline.com/2025/05/21/credit-scoring-gains-ground-in-ghana-amid-africas-digital-finance-shift/

Further Africa : https://furtherafrica.com/2025/09/24/ai-credit-scoring-unlocking-africas-invisible-economy/